A bit over a month ago, I wrote about the potential impacts of the then-looming fuel crisis on the tuna industry. Unfortunately, things have not got better.

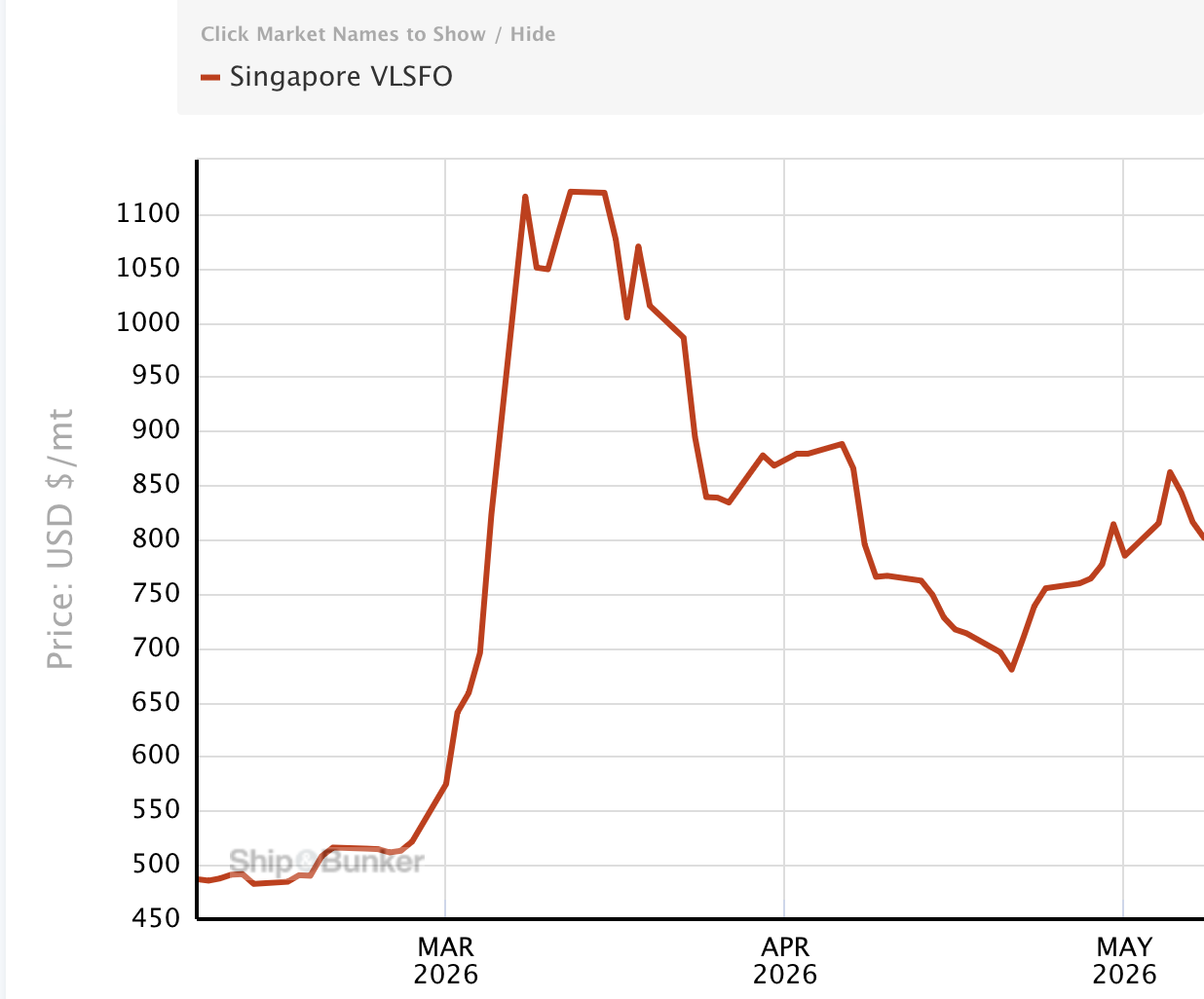

Source: https://shipandbunker.com/prices/apac/sea/sg-sin-singapore

When analysts discuss threats to global tuna supply chains, the usual suspects appear: overfishing, IUU fishing, climate change, labour standards, traceability gaps, and so on. These are real concerns. But the single biggest disruptor on the desk of every Pacific tuna vessel operator is none of them. It is a fuel invoice.

What began as military strikes between Israel, the US, and Iran has escalated into a full maritime crisis — Gulf shipping attacks, Strait of Hormuz restrictions, and the Houthis re-emerging as a force capable of paralysing Red Sea commerce. Most people read war headlines. Pacific tuna businesses are reading them as cost projections.

Here is the number that matters: Singapore bunker fuel — the benchmark for Pacific fishing fleet operations — was trading at USD 709 per tonne at the end of February. By 10 April, it had reached USD 1,630. Fuel prices doubled in six weeks.

This is not a minor fluctuation in input costs. Fuel accounts for 40 to 65 per cent of vessel operating costs in tuna fisheries. No other single variable comes close. When the Persian Gulf destabilises, Singapore’s crude supply tightens almost immediately — and the Pacific, which depends on Singapore for bunker fuel, feels the impact within days. The distance between a military strike in the Strait of Hormuz and a vessel operator in Majuro delaying departure is shorter than most people in this industry appreciate.

Fish prices have risen in response — skipjack has moved from around USD 1,600 to USD 2,000 per tonne — but nowhere near enough to offset the cost shock. Operators are caught in a margin squeeze with no quick way out.

What does a fleet do when fuel economics break down? It does not stop immediately. The changes are operational and incremental: dry-docking brought forward, port stays extended, departures delayed while waiting for price signals. By the third week of April, contractions were visible. Philippine fleets slowed. Taiwanese vessels lingered in port. South Korean ships returned early, nominally for maintenance. In fisheries economics, these are leading indicators. The supply chain notices them weeks later, often after the damage has already compounded.

The industry that worries me most in this scenario is not the large distant-water fleets backed by conglomerates or state subsidies. Those operations have balance sheets capable of absorbing a prolonged shock, and some have government support mechanisms that effectively socialise the risk. The operations that cannot wait out a six-month fuel crisis are the marginal domestic operators in Pacific Island countries — smaller fleets, thinner capitalisation, higher exposure to local financing costs, and far less resilience to external shocks they cannot influence.

When domestic Pacific fleets stop fishing, the consequences quickly move ashore. Processing plants in the Solomon Islands and Papua New Guinea depend on local tuna throughput. Reduced throughput generally means reduced employment, reduced export earnings, and direct pressure on foreign exchange reserves in economies where fisheries revenues are not marginal — they are foundational. A conflict in the Persian Gulf becomes, within months, a budget problem in Noro, in the Solomon Islands.

For me, this is the structural lesson that Pacific tuna fisheries policy (and surely others, too) struggles to grasp: global seafood systems are energy systems first. We spend enormous effort debating reference points, the use of dFADs, paying for Ecolabels, EM and observer coverage, catch documentation, labour standards, market access, and so on— all of it important, all of it necessary — yet fuel prices underlie everything.

Without affordable fuel, vessels don't move, carriers don’t transport fish, containers don’t get loaded, refrigeration chains become economically unviable, air freight costs escalate, and the access fee negotiations that underpin Pacific Island government revenues look completely different at the table, where distant-water operators factor fuel costs into every offer.

That last point deserves serious attention from Pacific governments. Prepaid vessel-day arrangements currently offer some insulation. But if high fuel prices persist through the next negotiating cycle, operators will build that uncertainty into their pricing. Nobody wants to pay yesterday's access fees against tomorrow's fuel bill.

There is a deeper paradox here. The foreign distant-water fleets that Pacific Island nations have, entirely reasonably, sought to regulate and extract greater value from are, structurally, better placed to survive this kind of shock than the domestic industries those same nations are trying to build. External shocks rarely first weaken the most powerful actors. They weaken the most exposed.

The tuna is still in the water. The vessels can still catch it. The market still wants it. But between the tuna and the plate lies a global logistics and energy system that is becoming increasingly volatile and more expensive to operate. Pandemics, conflicts, sanctions, climate disruption, freight crises — these are no longer exceptional events for Pacific fisheries managers to plan around. They are becoming the baseline operating environment.

The sector is no longer just managing tuna stocks; it is managing volatility. That requires a different kind of thinking from the one most fisheries institutions we work with were built for.